Talk to us

Talk to us Investment Management

The $4 Trillion Question: Does the Coming IPO Wave Change the Market Math?

July 1, 2015

Aspiriant News

Aa

Aa

Over the past year, the market has had difficulty assessing the magnitude of financial tremors emanating from epicenters around the planet. As a result, we have experienced exaggerated vibrations and aftershocks triggered by seemingly insignificant news and minor events. Importantly, we don’t believe any of the tremors coming from Greece, China or Puerto Rico are capable of wreaking market-wide havoc. However, we do believe tremors may become a more frequent occurrence as global growth remains generally subdued, interest rates remain low and increasingly volatile, and asset valuations are decidedly optimistic. This creates an environment characterized by lower investment returns and a market more prone to disappointment, all of which contributed to some of the exaggerated vibrations and volatility spikes we witnessed near the end of the second quarter. Indeed, this is proving to be the case thus far in 2015 as the S&P 500 Index has had the greatest number of one-percent daily moves since 2011. Even with the increased daily volatility, the S&P has been range bound between +/- 3.5% of its 2014 closing value.

After strengthening earlier this year, the U.S. dollar sold off relative to the Euro and Pound during the quarter. This helped International Developed Equities (MSCI EAFE Index) and Emerging Markets Equities (MSCI EM Index) maintain their edge against U.S. equities, gaining .6% and .7%, respectively during the quarter. The Treasury yield curve increased during the quarter with 10-year rates increasing by 41 basis points from 1.94% to 2.35%. As a result, bond returns were negative during the quarter, especially for longer maturity and higher yield bonds (bonds believed to have a higher level of investment risk). Meanwhile, Real Estate Investment Trusts (REITs) and Master Limited Partnerships (MLPs) struggled during the quarter, selling off by 6.8% and 6.1% respectively. Both of these asset classes were hurt by the shift in market yields as they tend to be more interest rate-sensitive over short periods of time than traditional equity investments. Commodities finally rebounded, up by 8.7% during the quarter despite the selloff in oil prices towards the end of quarter. Table 1 below details how some of the major market indices performed during the quarter, as well as their annualized trailing total returns.

EquitiesQ2YTD3YR5YR10YR

Table 1Major Index and Currency Performance

|

|||||

| Annualized Trailing Total Return | |||||

| S&P 500 TR | 0.3 | 1.2 | 17.3 | 17.3 | 7.9 |

| Russell 2000 TR | 0.4 | 4.8 | 17.8 | 17.1 | 8.4 |

| MSCI EAFE NR | 0.6 | 5.5 | 12.0 | 9.5 | 5.1 |

| MSCI Emerging Markets NR | 0.7 | 2.9 | 3.7 | 3.7 | 8.1 |

| MSCI All Country World Index NR | 0.3 | 2.7 | 13.0 | 11.9 | 6.4 |

| Fixed Income | |||||

|---|---|---|---|---|---|

| Barclays US Aggregate Bond TR | -1.7 | -0.1 | 1.8 | 3.3 | 4.4 |

| Barclays Municipal TR | -0.9 | 0.1 | 3.1 | 4.5 | 4.5 |

| Barclays High Yield Muni TR | -3.0 | -1.9 | 4.4 | 6.5 | 4.6 |

| Currencies | |||||

| Euro (EUR vs. USD) | 3.7 | -7.9 | -4.2 | -1.9 | -0.8 |

| Pound (GBP vs. USD) | 5.9 | 0.9 | 0.1 | 1.0 | -1.3 |

| Yen (JPY vs. USD) | -2.0 | -2.0 | -13.3 | -6.3 | -1.0 |

| Real Assets | |||||

| S&P GS Commodity Index TR | 8.7 | -0.2 | -10.7 | -4.3 | -6.2 |

| Wilshire Global Real Estate Securities Index TR | -6.8 | -2.5 | 10.0 | 14.2 | 6.8 |

| Alerian MLP TR | -6.1 | -11.0 | 7.8 | 11.5 | 11.4 |

Indices are unmanaged and have no fees. An investment may not be made directly in an index. Index returns shown are based in US dollars.

Economic recovery across the broader Eurozone is continuing to take hold (with the one obvious notable mention below). Retail sales across sectors throughout Europe increased during Q2, followed by an improving Purchasing Managers Index. Low levels of inflation are supporting real household incomes, and unemployment rates continued to fall during the quarter. As a result, consumer confidence is gaining momentum, and we believe consumer spending will lead to a stronger recovery during the second half of the year.

The recovery is supported by the European Central Bank (ECB), which remains committed to implementing the massive quantitative easing (QE) program it launched in January1. The ECB’s General Council confirmed the Eurozone recovery was “broadly on track,” but acknowledged potential downside risks. The Council further reiterated that their expectations for a continued recovery were contingent upon the ECB fully implementing the QE program, along with carrying out various policy measures. Furthermore, there is a reasonable chance the program will be extended in response to sluggish growth and/or low inflation.

Last year we recommended unwinding the underweight to the MSCI EAFE Index, which includes the Eurozone. Thus far, that decision has been a contributor to positive performance in 2015, which we expect to continue for the next several years. While we are pleased with this decision, as long-term investors we don’t get overly preoccupied with short-term results. Moreover, while we expect positive performance over the long-term, we also expect occasional fits and spurts along the way.

According to Trading Economics data, as of December 2014, Greece’s Gross Domestic Product (GDP) was $237 billion, representing just 1.6% of the European Union’s (EU’s) consolidated GDP of $14.5 trillion and just .3% of worldwide GDP. Aggregate sovereign debt in Greece is $320 billion, which is the highest debt load,2 the country has ever carried, even during the Global Financial Crisis. As part of its bailout package in 2010, the EU forced the country to accept austerity measures that significantly reduced government spending and simultaneously increased taxation (both personal and corporate). As we have written3, austerity has the noble goal of balancing budgets to reduce national deficits. However, implementing austerity during an economic contraction is akin to going on a crash diet in the midst of a famine, and more often than not, it turns out to be an ill-conceived diagnosis that can further exacerbate atrophy.

…implementing austerity during an economic contraction is akin to going on a crash diet in the midst of a famine…

Regardless of its ailments, we’re uncertain as to whether or not Greece will indeed secede from the EU. However, we have two thoughts on the subject:

In addition to the attention being given to Greece, more recently China took center stage. Before describing what happened, we need to provide some relevant context. Publicly traded companies in China are listed and trade as one of two options:

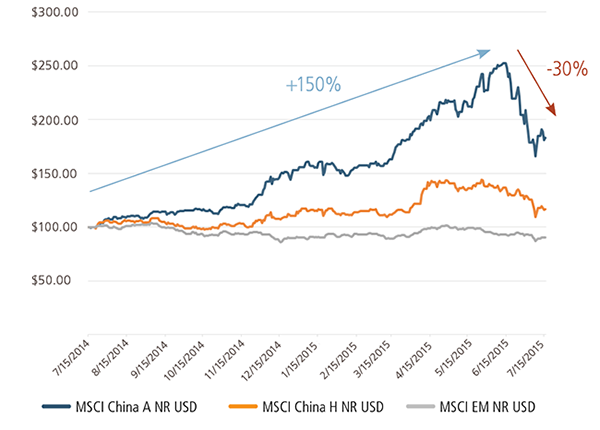

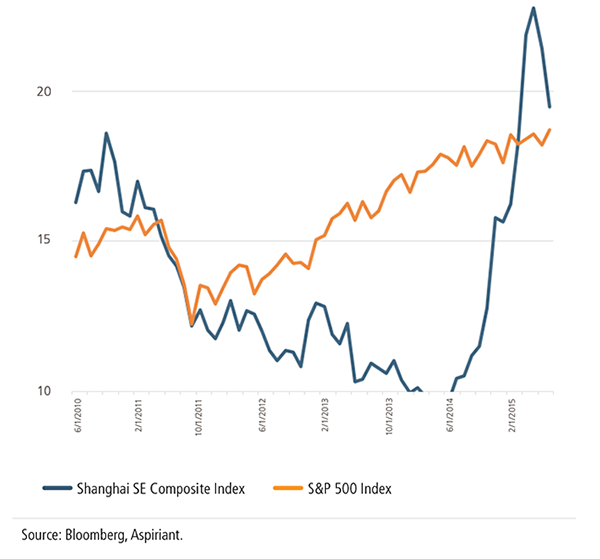

The huge run-up and recent drop in Chinese equities, which the media has been highlighting, occurred in mainland China on the Shanghai and Shenzhen exchanges (A-shares), while the (H-shares) performance has been substantially less volatile. As shown on Chart 1, the A-Shares soared approximately 150% in the 12 months from July 2014 through June 2015. Since then, they have fallen more than 30%, losing a combined $2.3 trillion in market capitalization in just four weeks. To put that in perspective, it is more than the entire market capitalization of France ($2.1 trillion) or Canada ($2.0 trillion). While that is a significant movement, we believe the A-Shares had run well beyond fair value and were, therefore, due for a correction. Chart 2 compares the price-to-earnings ratios of the Chinese A-Shares versus the S&P 500. We do not currently purchase A-shares. Moreover, our recommended global balanced portfolio5 has been underweight China for the past several quarters, with only 2% allocated to the H-Shares

Investment Growth (7/15/14–7/16/2015)

Price-to-earnings ratio

According to data from Trading Economics, China’s GDP in 2014 was approximately $10.4 trillion, second only to the U.S. at $17.4 trillion. Given the country’s significant role in global growth, a free fall in the Chinese stock market could threaten the prosperity of its consumers and, therefore, have a much broader impact around the world.

While we have been guarded about China’s cyclical industries (real estate, materials, financials), the amount of leverage and State Owned Enterprises (SOEs), we are generally less concerned about any fallout from a correction in Chinese equities on the real Chinese economy. Despite the recent collapse, the Shanghai Index is still up near 80% from levels one-year ago. Additionally, the rapid run-up in equity values was not correlated with increased consumption, so we don’t think a fractional decline will necessarily lead to decreased consumption. What’s more, the volatility in China (and specifically in the A-Shares) does not seem to be affecting other Emerging Market countries held within the index (see Chart 1).

As a back stop, the Chinese government has rolled out a series of policy measures to mitigate a potential collapse. Effective in June, Chinese pension funds may now invest in local equities. Additionally, bank reserve ratios and benchmark lending rates have been lowered along with other policies to help reduce questionable equity trading on the mainland exchanges.

It seems strange to us that the term “soft landing” is rarely used to describe the cooling of the U.S. economy from its significant recovery over the past several years. Instead, the term is typically reserved for potentially more treacherous situations like China. Nevertheless, after six years of recovery from March 2009 through March 2015, it seems clear the U.S. has experienced a soft landing. Table 2 shows the consensus GDP forecasts from the Federal Open Market Committee (FOMC) over the past five years. As shown, in four of the five years, the FOMC forecasts overestimated the actual growth experienced in the U.S. This doesn’t surprise us, since we think GDP growth will likely slow to less than 2% per year over the next few years. In fact, with falling energy prices and a strong U.S. dollar, we would not be surprised to see 2015 come in at less than 2%, but we’ll all have to wait until Q1 2016 to get a final tally.

Table 2Federal Reserve Forecast of US GDP1

|

||

| Year | Consensus2 | Actual |

|---|---|---|

| 2010 | 3.2 | 2.7 |

| 2011 | 3.7 | 1.7 |

| 2012 | 2.5 | 1.6 |

| 2013 | 2.7 | 3.1 |

| 2014 | 2.9 | 2.4 |

| 2015 | 2.5 | |

| 2016 | 2.5 | |

| 2015 | 2.2 | |

Source: Federal Reserve Board. Economic Projections of Federal Reserve Board Members and Federal Reserve Bank Presidents, March 2015.

(1) Measured as the median central tendency, excluding the three highest and three lowest projections for each year.

(2) Measured from the fourth quarter of the previous year to the fourth quarter of the year indicated.

In the meantime, we have received plenty of good news regarding the stability of the U.S. economy. The labor market has improved. In fact, the latest Beige Book published by the Fed reported labor shortages in several districts, while four districts noted difficulty retaining employees. In addition, higher wages were cited in some industries as well as a willingness by employers to increase wages in order to attract and retain workers. On a consolidated basis, the unemployment rate in June was at 5.3%. However, the labor force participation rate has declined in recent years to 63%, from a level of 65–66% between the late 1980s and late 2000s.

Other encouraging economic news included:

On the other hand, Wall Street’s avidly watched fear gauge, known as the Vix, spiked to its highest level in months, suggesting more turbulence ahead. Puerto Rico needs to restructure $72 billion in public debt. Many hedge funds began purchasing Puerto Rico’s bonds in recent months with the hope/speculation that they would recover. We have almost no exposure to Puerto Rican bonds, either in hedge funds or in our municipal bond managers.

Over the past several quarters, we have expressed our concerns about prevailing valuation levels as well as our expectations for increased volatility going forward6. In short, we believe most investors should currently hold portfolios that are modestly defensive (e.g. tilted towards risk managed equities with a meaningful allocation to bonds), and over the past year we have been making this recommendation. As markets continue to drift upwards and the impact of central bank intervention in this country and abroad wanes, our concern intensifies.

In short, we believe most investors should currently hold portfolios that are modestly defensive…

For over six years, ultra-low interest rates have enticed investors into taking more risk than normal as they search for ways to enhance the negligible returns of short-term, risk-free assets. This rising tide of liquidity has lifted the value of all assets and has been a significant source of positive financial market performance. Moving forward it’s difficult to believe valuation changes from current levels will result in a similar outcome. Valuations using the Shiller Price Earnings Ratio (Shiller PE) of the S&P 500 have doubled over the last six years, giving us a significant portion of our return during this period of time. We cannot and do not expect this to continue, forcing us to have lower return expectations moving forward despite how rosy the US markets currently appear relative to other parts of the world. For example, the Shiller PE is currently at 27 times earnings and has only crossed the level of 25 times earnings twice before – in 1926 and 2000.

Since the launch of the U.S. QE programs, the Federal Reserve’s balance sheet has quintupled from $895 billion in December 2007 to $4.5 trillion as of January 2015. Rightfully so, concerns have been raised about what will happen when the extraordinary measures come to an end and we return to more normal monetary policy. We believe the exit route from QE may take longer and be less hazardous than many investors expect. We believe the Fed will do its utmost to orchestrate an organized and sensible exit from QE. Therefore, we don’t necessarily believe an unwinding will result in spiking rates, inflation or unemployment. We continue to allocate capital in a manner that reflects these views and to invest in sectors where we expect the most attractive long-term, risk-adjusted performance.

1For a broader discussion on the ECB�s QE program, see our Q1, 2015 Insight.

2Debt load is defined as the aggregate amount of outstanding sovereign debt divided by GDP.

3For a broader discussion on the impact of austerity measures, see our Q1, 2014 Insight.

4MSCI recently announced that it is considering the Chinese A-Shares for inclusion within the MSCI Emerging Markets Index, which could occur before year-end.

5Global balanced portfolio represented as 60% allocated to equities benchmarked against the MSCI All Country World Index and 40% allocated to bonds benchmarked to the Barclays Municipal Bond Index.

6For a broader discussion valuations and expected volatility, see our Q1 2015 Insight.

Important disclosures: Past performance is no guarantee of future performance. All investments can lose value. Indices are unmanaged and it is impossible to invest directly in an index. The volatility of any index may be materially different than that of a model.

Equities. S&P 500 is a market-capitalization weighted index that includes the 500 most widely held companies chosen with respect to market size, liquidity, and industry. The Russell 2000 Index measures the performance of the small-cap segment of the U.S. equity universe. It is a subset of the Russell 3000 Index representing approximately 10% of the total market capitalization of that index. It includes approximately 2000 of the smallest securities based on a combination of their market cap and current index membership. The MSCI EAFE Index (Europe, Australasia, Far East) is a free float-adjusted market capitalization index that is designed to measure the equity market performance of developed markets, excluding the US & Canada. The MSCI Emerging Markets Index is a free float-adjusted market capitalization index that is designed to measure equity market performance of emerging markets. The MSCI ACWI Index is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed and emerging markets.

Fixed Income.The Barclays U.S. Aggregate Index represents securities that are SEC-registered, taxable, and dollar denominated. The index covers the U.S. investment grade fixed rate bond market, with index components for government and corporate securities, mortgage pass-through securities, and asset-backed securities. These major sectors are subdivided into more specific indices that are calculated and reported on a regular basis. The Barclays Municipal Bond Index is a rules-based, market-value-weighted index engineered for the long-term tax-exempt bond market. The index has four main sectors: general obligation bonds, revenue bonds, insured bonds, and prerefunded bonds. The Barclays High Yield Municipal Bond Index is an unmanaged index composed of municipal bonds rated below BBB/Baa.

Real Assets. S&P GSCI: The S&P GSCI© is a composite index of commodity sector returns representing an unleveraged, long-only investment in commodity futures that is broadly diversified across the spectrum of commodities. The returns are calculated on a fully collateralized basis with full reinvestment. Wilshire Global RESI is a broad measure of the performance of publicly traded global real estate securities, such as Real Estate Investment Trusts (REITs) and Real Estate Operating Companies (REOCs). The index is capitalization-weighted. The Alerian MLP Index is a gauge of large and mid-cap energy Master Limited Partnerships (MLPs). The float-adjusted, capitalization-weighted index includes 50 prominent companies and captures approximately 75% of the available market capitalization.

Want the latest wealth management tips, investment insights and Aspiriant news delivered straight to your inbox. Sign up for regular Fathom updates so we can send you the most relevant content you selected below.