Talk to us

Talk to us Wealth Planning

The Financial Questions AI Employees Are Asking Behind Closed Doors

August 26, 2020

To defend against uncertainties related to soil quality, rain and temperature, successful farmers try to increase yield by planting and rotating their crops. Similarly, professional investors attempt to improve performance through diversification and shifting allocations.

Our Capital Market Expectations (CMEs) provide a framework for understanding how asset classes are likely to perform in the years ahead. However, policymakers can influence the outcomes by introducing fiscal and monetary stimulus, which carries significant implications for investors. While we see mounting risks in some areas, we are finding attractive opportunities elsewhere.

Given the wide range of uncertainties, we expect our broadly diversified portfolios to perform reasonably well, regardless of the environment. However, we may soon rotate our allocations, accentuating asset classes we believe will enhance yield while maintaining our overall defensiveness.

Social distancing is one of the most effective tools when it comes to curbing health pandemics. While necessary to combat the virus’ spread and preserve life, it has had important short-term and long-term implications about which investors should be aware.

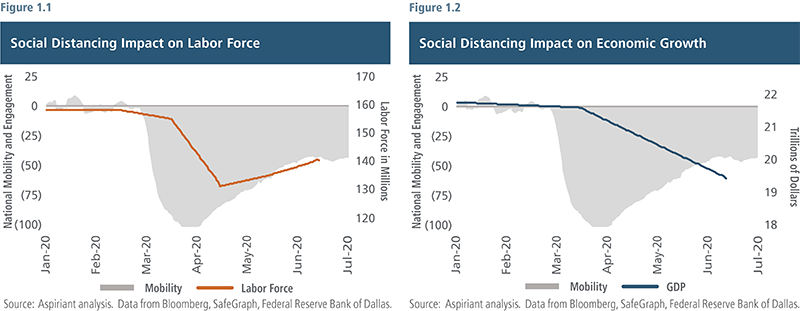

The gray shaded areas in Figures 1.1 and 1.2 attempt to capture the level of social distancing across the United States. The orange line in Figure 1.1 reflects the country’s employed workers or labor force. The blue line in Figure 1.2 shows the country’s economic growth, or Gross Domestic Product (GDP).

During the first two months of the year, socialization was more-or-less normal. By March, governments across the country began mandating business and agency closures as well as shelter-at-home orders. The combined impact of those directives is reflected by the sharp, downward dip in social mobility. Business disruptions reduced the need for employees, leading to record-setting terminations, layoffs and furloughs. More than 50 million Americans have filed initial jobless claims thus far in 2020.

Although social distancing has lessened since the depths in March and April, interactions certainly haven’t returned to normal. In fact, an upward trend in new coronavirus case counts, hospitalizations and deaths over the past several weeks caused many states and cities to delay re-opening plans. Moreover, millions of people elect to continue following social distancing standards for their own safety. As a result, social interaction may remain below normal, possibly for quite some time into the future.

The net effect is the country currently has about 15 million fewer workers (consumers and taxpayers) than it did coming into the year. Income loss and uncertainty have weighed on consumption, which can exacerbate and prolong the downturn. In fact, we’re expecting a contraction of 6.8% in year-over-year GDP. Moreover, we don’t expect a return to pre-pandemic GDP until 2022.

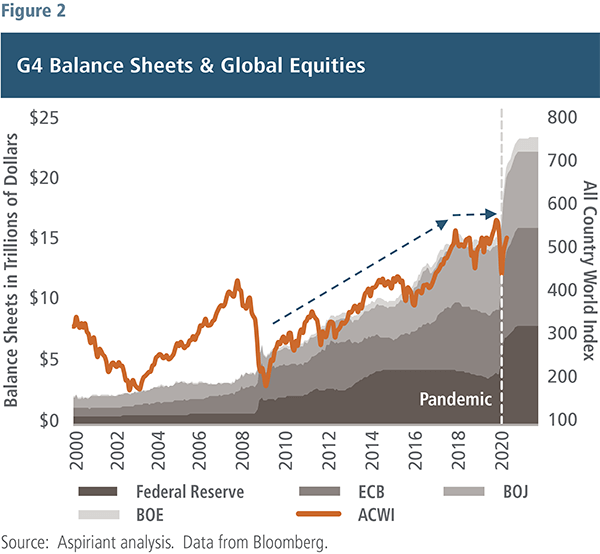

Neither the employment nor growth pictures above can be described as a v-shaped recovery. So, why then have financial assets recovered so quickly? We believe massive fiscal and monetary stimulus is the answer.

To spur borrowing and spending, every developed market central bank anchored short-term interest rates at, near or even below 0%. Additionally, central bank actions have also driven long-term (e.g. 10-year) interest rates well below 1%. Since interest rate levels were already low coming into the crisis, these marginal post-crisis reductions have done little to encourage new borrowing, particularly for households and consumers. As a result, the impact on the economy through spending on goods and services has been minimal. However, the additional liquidity has had a pronounced effect on financial markets. The purchase of government securities and other assets by central banks, known as quantitative easing (QE), has prompted a movement out of low-yielding securities into higher returning securities, like credit and equities, fueling the rally over the past several weeks.

Throughout the world, policymakers deployed mind-boggling deficit spending programs designed to help alleviate the economic hardships faced by individuals and businesses. The gray shaded areas in Figure 2 display the assets (largely government securities) held by the Federal Reserve, European Central Bank, Bank of Japan and Bank of England. In aggregate, the banks held just $3 trillion in assets prior to the Global Financial Crisis (GFC) in 2008. Then, their assets rapidly increased, quintupling to $15 trillion over the next decade as the banks gobbled up financial assets in an effort to stabilize and support their economies and markets. In response, global equities (orange line) tripled in market value between March 2009 and December 2019.

With the onset of the global pandemic (vertical dashed line), these central banks collectively pledged an additional $8 trillion in market support over the next two years. With greater scale and an accelerated deployment of central bank purchasing, equities have roughly reclaimed their pre-pandemic levels.

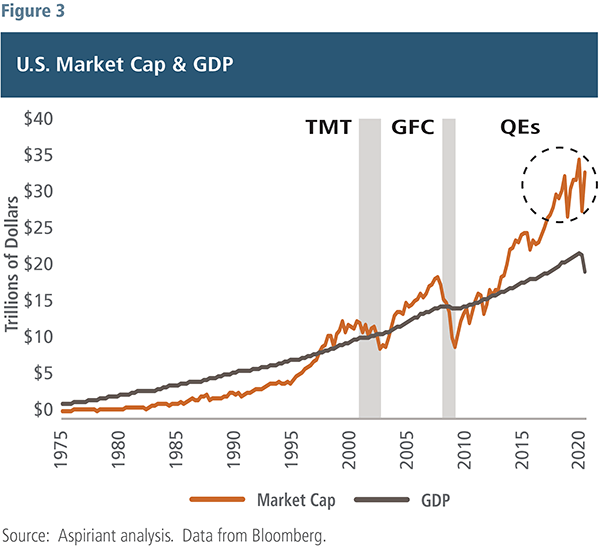

While virtually all financial assets benefit from stimulus-induced risk-taking, U.S. equities seem to have responded best. Figure 3 illustrates that the size of the overall U.S. economy has been a good predictor of the long-term trend in the value of the country’s publicly traded companies. That’s intuitive since the companies themselves account for a significant portion of the nation’s business activity. Therefore, their market values should reflect the trajectory of the economy.

During three periods of elation — the technology, media and telecommunications bubble (TMT); GFC; and QEs — investors bid up the current market value, and therefore the expected earnings, of the companies, causing their equity values to break well above trend. Each of the first two periods crashed with devastating effects. In fact, from peak to trough, investors lost 49% of their money during the TMT and 57% during the GFC.

As shown in the dashed circle, equities sold off twice during the current QE period. The first was during the fourth quarter of 2018 when the Fed was lifting interest rates, and the second was during the first quarter of this year as the pandemic began to take hold. In the weeks following the onset of COVID-19, the Fed rapidly flooded markets with a level of liquidity that had taken years to reach during the GFC. In both instances, Fed policy was the catalyst for the market reversals. Going forward, the Fed’s actions may be less helpful in reversing a market drop given the practical limits of money printing, inflation and/or currency weakness.

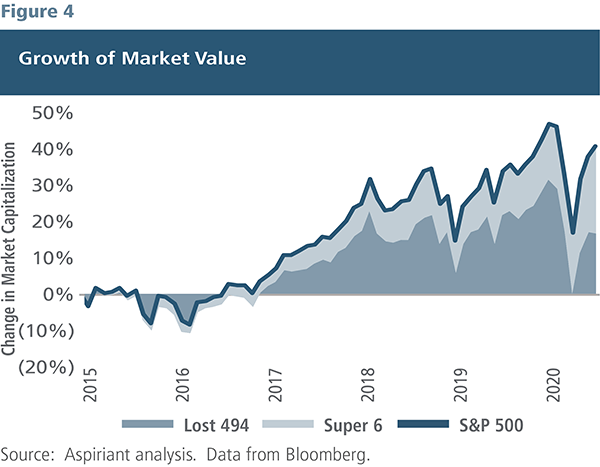

Upon closer examination, the departure from economic reality has really been driven by just six stocks: Facebook, Apple, Amazon, Netflix, Google and Microsoft. Figure 4 separates those six companies from the remaining “Lost 494” companies in the S&P 500 index. Many of these lost companies are terrific businesses that have enjoyed and endured decades of both good and bad economic environments. They include Berkshire Hathaway, Johnson & Johnson, Merck, Procter & Gamble, Clorox, Coca-Cola, PepsiCo, Intel, Verizon, AT&T, Visa, Mastercard and JPMorgan.

Over the past five-and-a-half years, the S&P 500 generated a cumulative return of 40% — increasing in market value by $7.3 trillion. Of that amount, more than half, $4.6 trillion, came from just the Super 6 stocks.

After years of investors concentrating in these six top companies, their stocks currently represent 25% of the S&P 500’s overall market value, exceeding the previous record of 18% set by the corresponding six largest stocks just prior to the sell-off in the TMT bubble. To further put this into perspective, the market cap of the Super 6 exceeds the GDP of every country outside of the U.S. — save for China.

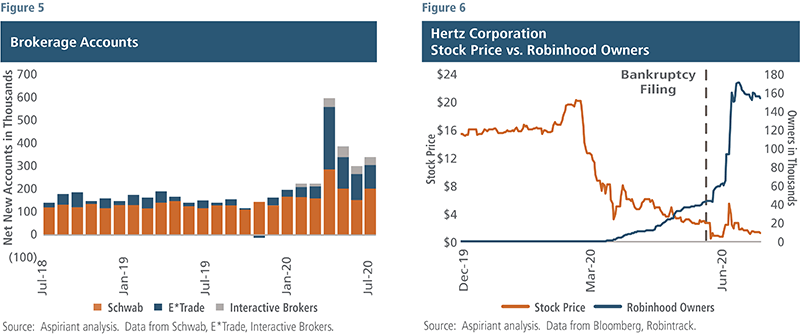

In addition to generous amounts of fiscal and monetary stimulus, a swarm of day traders has also caused distortions in the financial markets. Toward the end of 2019, some of the largest consumer brokerage platforms moved to zero commission trades, removing a trading cost. As the health pandemic began to spread in early 2020, elected officials began suspending or otherwise restricting large social gatherings. These mandates led to suspension of professional and college sports, causing millions to seek another pastime.

As boredom set in, a number of first-time traders began opening accounts. Figure 5 shows the spike in net new accounts opened across three popular trading platforms: Charles Schwab, E*Trade and Interactive Brokers. Between March and June, more than 1.6 million accounts were opened across those three platforms — by far the highest total in any six-month period. In addition, millions of additional accounts were opened on other platforms, including Fidelity, TD Ameritrade and Robinhood.

Much of the recent activity could be described as speculative trading, rather than long-term investing. Figure 6 illustrates the point, but numerous such examples exist. The chart displays the stock price of rental car company Hertz versus the number of account holders on the Robinhood platform. Coming into the year, the stock dropped precipitously in anticipation of its bankruptcy filing, which occurred on May 22. While savvy investors such as Carl Icahn, who know the company well, bailed on the stock, retail investors who know very little about the company or the bankruptcy process began piling in. The massive upswing in account holders caused the stock to temporarily rally from a low of 55 cents on May 26 to $5.53 on June 8. On paper, some of these investors temporarily made 10 times their investment. But the win was short-lived as the stock has since settled at about $1.50. Moreover, the current price may be artificially high as the bankruptcy restructuring process could wipe out the entire value of the common equity.

Although difficult to track, these day traders have impacted market activity, especially for some highly recognizable Super 6 companies. For example, Goldman Sachs estimates that small options trades in Alphabet (Google’s parent company) account for nearly one-third of the total options trading. Moreover, same session round trips — in which an investor both opens and closes a position on the same day — have increased dramatically, especially in stocks like Apple.

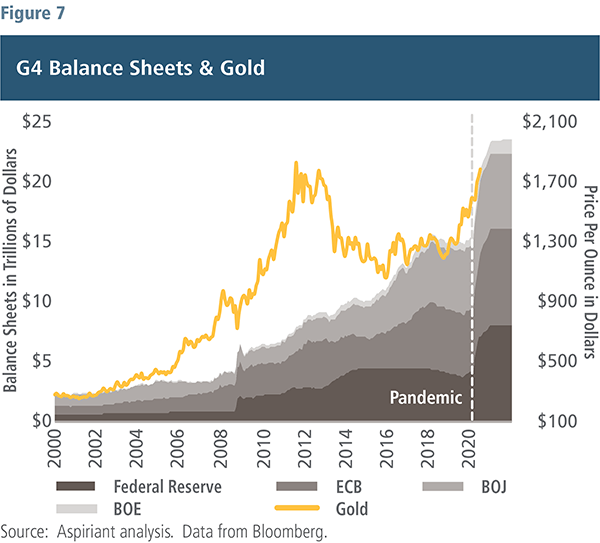

To correct the existing (and growing) incongruence between financial markets and economic fundamentals, one of two things needs to happen: Asset prices need to decline or earnings and cash flows need to grow over time to cause valuations to drift down to more normalized levels. One way for the latter scenario to unfold is for inflation to blossom and push nominal profits higher (while real or inflation-adjusted earnings remain reasonably stagnant). Inflation, dormant for much of the past 40 years, may seem like a remote possibility in the immediate aftermath of this crisis. But with trillions of dollars of stimulus sloshing around, inflation could rekindle over a longer time horizon. As such, investors would be well-served by holding some assets that are responsive to inflationary impulses that may emerge over the next few years. Gold, among others, is one of those assets.

Like equities and other assets, gold has benefited from the substantial infusion of liquidity provided by global central banks, as shown in Figure 7. Since the start of the year, the price of gold, as denoted by the yellow line and measured against the right vertical axis, has increased by as much as 35%, and currently trades at roughly $2,000 per ounce.

Investors expect central banks to continue adding trillions of dollars to their balance sheets, likely leading to rising inflation and/or a loss in confidence in paper currencies, the U.S. dollar explicitly. Since a lot of central bank asset purchases will be required to finance growing fiscal deficits, we expect these balance sheet expansions will more directly link to spending on goods and services, and as such, have more significant inflationary implications than what materialized during and after the GFC. Along those lines, inflation expectations have started to creep up since the start of the pandemic, with break-even inflation, or the difference in yields between nominal bonds and inflation-linked bonds like Treasury inflation-protected securities (TIPS), moving from 0.6% to 1.6% over the past few months.

The dollar, meanwhile, has also retreated a bit. Since March, the dollar is off 7% against a traded weighted basket of currencies.

Among the attractive features of gold is its limited production. Distinct from paper currencies, gold is a finite resource, and its supply cannot easily be manufactured by a simple electronic transfer. Over the past 20 years, the annual production of gold has equaled roughly 2% of existing supply. Substantial new discoveries are increasingly rare with production expected to become even more constrained in the years ahead. Long development timelines, remote sites with little surrounding infrastructure, and newly attuned concerns about destructive mining techniques are among the factors that will limit future production. In contrast, the money supply (defined as physical currency, demand deposits and checking accounts, as well as traveler’s checks) has increased by 8% per year, on average, since 2000, with more pronounced spikes around recessions.

The paradigm investors grew accustomed to for much of the last 40 years has largely run its course. Monetary policy and interest rates, in particular, were the principal mechanism for managing the economy, irrespective of whether the economy was above, at or below full capacity. With interest rates, hovering near zero and asset purchases well underway, fiscal policy must now take the lead and drive a sustained economic recovery. The scale, shape and duration of fiscal initiatives, however, are not fully known, with the November elections only adding another element of uncertainty. Unlike monetary policy, where decisions are made among a small circle of officials and largely independent of outside influences, political divisions will be more disruptive to the implementation of effective fiscal policy. Partisan bickering adds another dimension of complexity for investors to assess and can inject more volatility into markets.

With monetary policy, we kind of knew what needed to be done. Short-term interest rates, on average, had to drop about 5% in the face of an economic contraction to encourage more borrowing and prompt a virtuous cycle of more spending, higher incomes, more spending, higher incomes, and so on. With fiscal policy, particularly now, the potential outcomes are wider and less clear. Well-conceived, appropriately sized policy can lead to both higher economic growth and further reflation or gains in financial assets, equities most notably. Conversely, poorly designed or implemented, as well as insufficiently calibrated, policy for the existing circumstances could lead to stagflation (meaning high unemployment, low growth and high inflation). Even more concerning, we could see episodes of deflation or falling prices.

We believe the most sensible approach to this uncertainty is to hold a well-diversified portfolio that is resilient to a range of scenarios, both good and bad.

In that regard, we recommend resisting the temptation to be heavily concentrated in a narrow range of winning stocks. The Super Six are strong companies, no debate about that. But their size and success limit their ability to continue compounding shareholder returns at reasonable levels and put them in the spotlight of more government scrutiny, both here and in China as frictions between the countries escalate.

Value stocks appear set to have their day in the sun (see our accompanying supplement, Value Stocks: Ready to Grow). International markets, including emerging markets, continue to offer more inviting long-term opportunities given lower valuations. We think global diversification remains as important as ever, given the uneven health, economic and political responses to the coronavirus around the world. We would look to take advantage of market sell-offs to partially shift out of low or zero yielding assets to ones that offer higher spreads to cash. And finally, adding to positions in less correlated assets, like gold, that can hedge adverse outcomes, including inflationary and deflationary environments, provides needed ballast in a world of great uncertainty.

Important Disclosures

Aspiriant is an investment adviser registered with the Securities and Exchange Commission (SEC), which does not suggest a certain level of skill and training. Additional information regarding Aspiriant and its advisory practices can be obtained via the following link: https://aspiriant.com.

Investing in securities involves the risk of a partial or total loss of investment that an investor should be prepared to bear.

Any information provided herein does not constitute investment or tax advice and should not be construed as a promotion of advisory services.

The views and opinion expressed herein are those of Aspiriant’s portfolio management team as of the date of this article and may change at any time without prior notification. Any information provided herein does not constitute investment or tax advice and should not be construed as a promotion of advisory services.

Past performance is no guarantee of future performance. All investments can lose value. Indices are unmanaged and you cannot invest directly in an index. The volatility of any index may be materially different than that of a model. The charts and illustrations shown are for information purposes only. All information contained herein was sourced from independent third-party sources we believe are reliable, but the accuracy of such information is not guaranteed by Aspirant. Any statistical information in this article was obtained from publicly available market data (such as but not limited to data published by Bloomberg Finance L.P. and its affiliates), internal research and regulatory filings.

MSCI ACWI Index is a free-float weighted equity index representing both domestic and emerging markets. S&P 500 is a market-capitalization weighted index that includes the 500 most widely held companies chosen with respect to market size, liquidity and industry.

Want the latest wealth management tips, investment insights and Aspiriant news delivered straight to your inbox. Sign up for regular Fathom updates so we can send you the most relevant content you selected below.