Talk to us

Talk to us

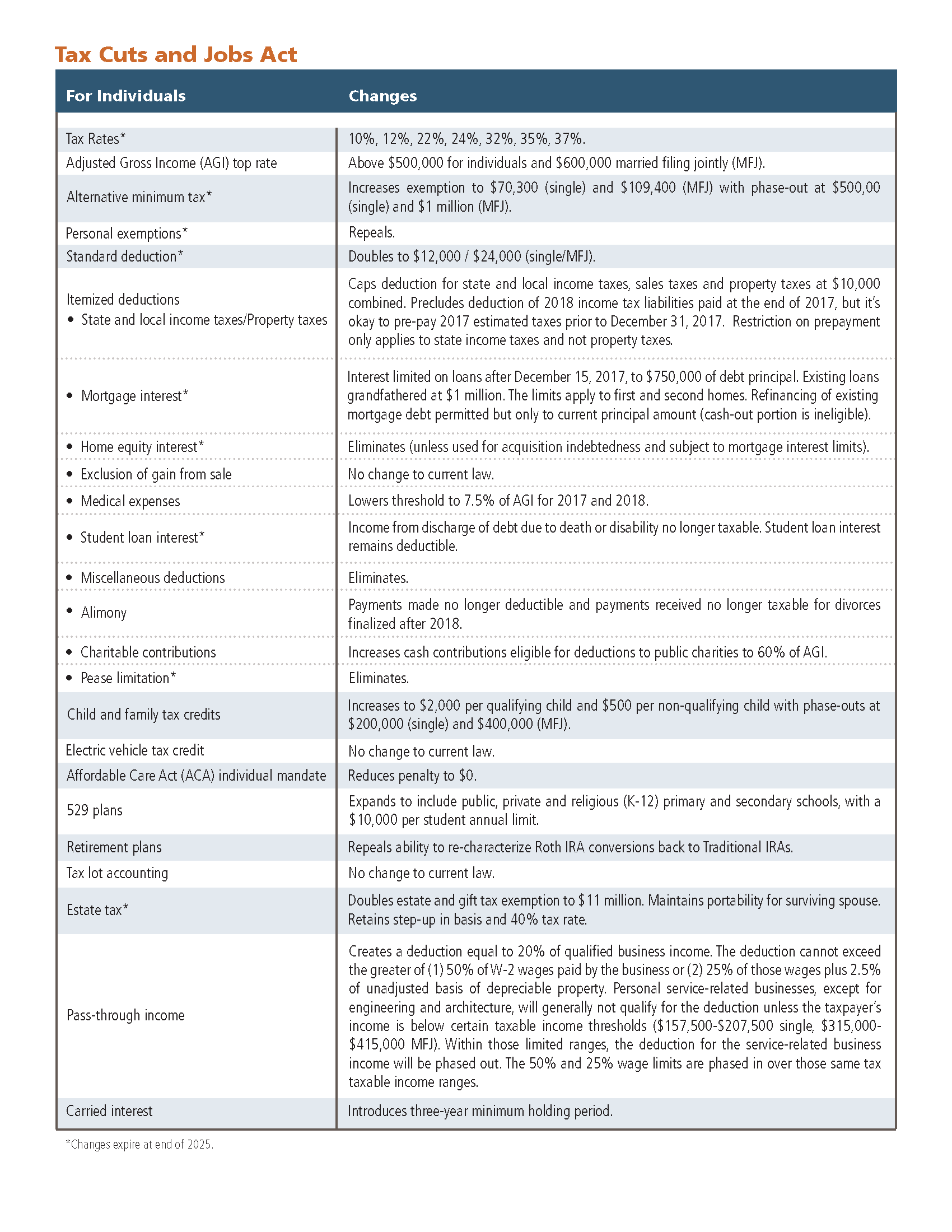

Following the passage of the Tax Cuts and Jobs Act (Tax Act) by both chambers of Congress, President Donald Trump signed the legislation in the final days of his first year in office. Almost all provisions of the Tax Act go into effect on January 1, 2018. As we absorb the contours and complexities of the legislation, we believe there is enough clarity around key provisions to share our preliminary assessments of the legislation.

Economic growth

Over the long term, we expect the net effect on economic growth to be fairly modest, with some quickening of growth impulses in the near years followed by periods of softer growth as some benefits sunset and budget gaps widen over time. The nonpartisan Joint Committee on Taxation1 and other organizations2 estimate that economic growth will accelerate by about 0.10% to 0.30% per annum over the next 10 years and fall short of the levels required to make the Tax Act revenue neutral.

For any bounce in economic activity to be sustainable, the supply of labor and/or capital must durably rise. Given the small decline in individual marginal tax rates (and offsets for many high-income earners), unemployment at multi-year lows, and skill gaps prevalent across many industries, we do not expect the total hours worked to meaningfully change in response to the Tax Act.

Capital spending implications, on the other hand, are much more difficult to assess. While leaving capital gain tax rates unchanged, the Tax Act offers several incentives — such as lower corporate tax rates, full expensing of capital expenditures, one-time repatriation tax on overseas profits and a territorial tax system — to encourage investment and grow the capital stock of the economy. Unfortunately, we cannot fully evaluate the probable effects of the Tax Act on capital formation as a number of difficult questions arise.

- Will companies commit to long-term capital projects in the ninth year3 of an economic expansion?

- Have remarkably low funding costs over the past several years already motivated companies to make most, if not all, productive investments?

- Will corporations mirror prior tax holidays4 and primarily use repatriated profits to pay down debt and repurchase shares?5

- Will rising federal budget deficits crowd out private investment opportunities and raise borrowing costs for companies?

In any event, it appears reasonable that any economic momentum attributable to the Tax Act is likely to be dulled by anticipated interest rate increases in the approaching months. With employment strong and inflation measures firming, particularly housing and cyclical services, the Federal Reserve now has additional justification to press ahead with further interest rate hikes and to cautiously unwind other measures taken in the aftermath of the financial crisis.

Lastly, we would attach a (non-trivial) possibility that the legislation could be unwound, either in part or in whole, before selected provisions would otherwise naturally expire. Historically, major legislation passed on a party-line vote is often not durable. Please see the Affordable Care Act (and the removal of the individual mandate as part of the Tax Act) as a reference. With one of the largest funding sources, the elimination of state and local tax deductions (SALT)6, weighing more heavily on traditional “blue” voting states, it is conceivable Democrats will try to neutralize the legislation and prevent an exodus of high-wage earners and jobs from their states. As such, we, regrettably, are conditioned for more brinkmanship/dysfunction in Washington, with attendant spells of periodic uncertainty relating to policy and governance in the months and years ahead. Should such policy uncertainty surface on taxes, we would expect the law’s intended benefits to be even more muted than initial estimates.

Equity markets

As expectations for the successful completion of the tax package spiked in recent weeks7, markets appear to have priced in most, if not all, of the near-term benefit. High-tax stocks or more domestically oriented shares outperformed low tax stocks or more globally exposed business franchises in the weeks8 leading up to final approval of the Tax Act by the House of Representatives on December 20.

Five to 10 percent of this year’s market advance may be tax related, a move roughly equivalent to the estimated bump in earnings from lower net taxes.9 If near-term growth expectations edge upward or interest rates climb higher, then value stocks may come back in favor as investors rotate to more cyclical and less interest rate-sensitive assets. Conversely, more aggressive interest rate moves may pressure low volatility and dividend strategies as relative yield considerations shift. Finally, more equity issuance over time, resulting from new limitations on corporate interest deductibility, should not materially influence markets as any share dilution (higher share count) should be neutralized by lower risk premia (reduced volatility and higher multiples).

Inflation and interest rates

Significant fiscal stimulus late in the economic cycle, coupled with rising federal budget deficits, will likely raise inflationary pressures in the near term and keep the Federal Reserve normalization process on course. Without a dramatic spike in inflation, we expect interest rates to move gradually higher but settle below historical averages.

Municipal bonds

Municipal bonds, like other fixed income securities, tend to be adversely impacted by an unexpected rise in interest rates. We do not, however, believe that any upward move in interest rates, particularly on the long end of the curve, will be jarring to the municipal bond market as those increases are most probably absorbed over time.

The reduction in marginal tax rates may make the after-tax income opportunities for some investors (e.g., corporations, selected individual investors) less attractive. But for others, notably those in states that will lose the SALT deduction, municipals will become even more appealing. As mentioned above, an issue to watch closely is the net migration patterns of people in high-tax states (e.g., Calif., N.Y., N.J.) as jobs potentially shift to lower cost areas. Many of these states are disproportionately reliant on taxes from high-income filers, so even a small migration effect could have a pronounced impact on a state’s fiscal position and the credit quality of its municipal bonds. Additionally, property values in many of these same states should come under some pressure and encumber future efforts to repair budget shortfalls.

Credit markets

With repatriated overseas cash subject to a one-time tax of 15.5% and future overseas earnings untaxed (even if brought back to the U.S.), many multinationals will have less of a need to borrow to fund buybacks, dividends and other corporate activities. Moreover, the large reduction in the corporate tax rate to 21% from 35% reduces the value of the interest tax shield, making the after-tax cost of debt more expensive. Accordingly, the supply of investment grade bonds may decline over time, narrowing credit spreads and boosting returns.

High yield credits will face more uncertainty as the limit on corporate interest deductibility captures a much larger percentage of the market. The Tax Act curbs interest to 30% of adjusted taxable income (ATI) plus business interest income (depreciation and amortization expenses are added back to ATI until 2022). Some lost interest deduction is offset by the lower corporate tax rate, as well as the expensing provisions that allow companies to immediately deduct the entire cost of new capital investments.

One unforeseen consequence of these changes is the asymmetric impact across different economic settings. Specifically, any adverse impact is more heavily borne in a deteriorating economy as more companies become subject to the interest rate caps (and are further exacerbated by the elimination of net operating losses carrybacks). While the impact on credit quality is difficult to assess immediately, we do expect, as in the investment grade market, lower high yield debt issuance over time with equity representing a higher share of the capital structure.

On balance, the impact of the legislation on the high yield market should be manageable with any turbulence and return dispersion concentrated in the lower quality, more highly leveraged names.

Real estate and housing

Commercial real estate should hold up fairly well as many proposed changes keep current conventions in place or provide a slight benefit. The corporate interest deduction limit does not apply to real estate companies, and REIT dividends and rental income are now eligible for the lower pass-through rates. The Section 1031 deferral of gain recognition on like-kind exchanges, which was discontinued for personal property, remains in place for real property. Multifamily assets, assuming state and local governments can avert large out-of-state job migration in high-tax areas, should gain an advantage in expensive coastal areas as home affordability deteriorates due to the lost SALT deduction, curtailment of mortgage interest deductibility, and the increased standard deduction. Retailers, and by association their landlords, should get a boost from a lower corporate tax rate, but pressure from internet competitors will continue to impair physical merchants and most retail assets.

In summary

The first-order effects of the tax legislation on various asset classes are fairly neutral. Some gains and some losses, but on the margin, virtually all are modest. Secondary and tertiary effects will take time to surface as details emerge and behaviors change. Undoubtedly, there will be unexpected outcomes and surprises. As taxpayers, corporations and the markets adjust to the changes brought by its passage, we will continue to update our perspectives on the Tax Act.

Footnotes:

1Joint Committee on Taxation, Macroeconomic Analysis Of The “Tax Cuts and Jobs Act” As Passed by the House of Representatives on November 16, 2017, December 11, 2017.

2Committee for a Responsible Federal Budget, “Can Tax Reform Generate 0.4% Additional Growth?” November 27, 2017.

3The National Bureau of Economic Research.

4Dhammika Dharmapala, C. Fritz Foley, and Kristin J. Forbes, “Watch What I Do, Not What I Say: The Unintended Consequences of the Homeland Investment Act,” National Bureau of Economic Research Working Paper No. 15023, June 2009.

5Bank of America Merrill Lynch Corporate Risk Management Survey, July 10, 2017.

6Joint Committee on Taxation, Estimated Budget Effects Of The Conference Agreement For H.R.1, The “Tax Cuts and Jobs Act,” December 18, 2017.

7PredictIt CORP.TAXCUT.2017.

8Financials, energy and industrials stocks outpaced technology and healthcare shares from November 1, 2017, to December 20, 2017.

9Goldman Sachs, 2018 US Equity Outlook: Rational Exuberance, November 21, 2017.