Talk to us

Talk to us Inside Aspiriant

Building What Lasts: Welcoming Aspiriant’s 2026 Partners

November 1, 2015

Aspiriant News

Aa

Aa

If you are an experienced investor, sooner or later, you come to understand what it means to be tested by the markets. When you see market sentiment so negatively affecting one of your portfolio positions you start wondering whether or not something has fundamentally changed, or maybe you missed something or misinterpreted a key variable.

We have asked ourselves those kinds of questions, and many more, over the last few months regarding our MLP exposure in client portfolios. We know that on occasion an investment may not work out as expected, and when that happens we seek to understand why so we don’t make the same mistake in the future. In the case of our MLP allocation, which clearly hasn’t produced the results we were expecting over the last year, we still believe our investment thesis remains intact. Moreover, we continue to think the long-term investment outlook for this asset class remains attractive and fairly unique in today’s capital markets.

Over the next ten years, we expect this asset class to follow a similar growth trajectory as real estate investment trusts (REITs) did throughout the 1990’s. We believe the asset class will mature, get larger and become more mainstream in investment portfolios because MLPs are a key component in the U.S. energy independence equation. We want our clients to participate in this real secular growth story and have positioned our portfolios accordingly.

The MLP sector is still in a formative stage of development, and its transformation into a more mature asset class with greater depth isn’t going to happen overnight. Bear in mind the modern MLP structure originated in the late 1980’s, index data is only available since the mid 1990’s, the market cap is still relatively small, the businesses are often misunderstood, and MLPs have a fair amount of tax complexity. Given the short history and limited data, it’s more challenging for this asset class to weather a storm of negative investor sentiment and a pessimistic financial press compared to more mature segments of the market.

Consequently, markets may, at times, exhibit a little more uncertainty in valuing these businesses, which just means there will be higher highs and lower lows along the way.

Despite a recent bump up in early October, we’re in one of those ‘lower low’ periods right now. Recent performance has been amongst the worst we’ve seen in the history of MLPs. Through the end of the third quarter, the 3-, 9- and 12-month performance of the Alerian MLP Index (in very round numbers) has been -20%, -30% and -40%, respectively. So we are deep into bear market territory for this asset class. As a result, on average the performance of MLPs has detracted approximately 2-3% from our model portfolios.

Anecdotally, we’ve heard of some forced selling on the part of levered investors, like hedge funds and closed-end mutual funds, and also some normal window-dressing1 activity from long-only managers selling before end of quarter reporting. We’re also seeing selling pressure come from less well-informed investors who are worried about distributions being cut or who may not fully understand how these businesses relate to lower oil prices, reduced drilling activity or interest rate fears from the Fed.

Adding some fuel to the fire, an analyst recently wrote an article in a widely read and respected weekly market journal suggesting the MLP operating structure may not survive, or that current distribution levels will ultimately prove unsustainable. When these opinions are expressed in mainstream publications, it lends some credibility to a bearish outlook even though the claims, we believe, are misleading and demonstrate a lack of understanding about how these businesses finance themselves and operate.

Although our view remains that markets tend to be informationally efficient most of the time, there are times when they can also be misinformationally efficient (i.e., prices reflect all available misinformation). We believe misinformation has probably added to the confusion and fear surrounding this asset class today.

Let’s address some of the more sensational assertions from the article:

“Most MLPs are dependent on external capital market assistance to fully fund the current levels of their distributions and dividends”

MLPs do rely on external capital, but only to finance growth initiatives – not to fund distributions. Distributions are in fact funded internally from the ongoing operations of the business. According to Barclays, the average distribution coverage ratio for the entire sector for 2016 is estimated to be 1.12, which means the average MLP is generating 112% of the cash they are distributing to investors from operations.

“Most MLPs will need to make a decision to cut distributions/ dividends or suspend growth”

Some MLPs have cut distributions, but they have been nontraditional partnerships that our client portfolios do not own. According to Kayne Anderson, some upstream2 MLPs have suspended growth in 2015 and 2016 given the sharp decline in commodity prices and the corresponding pull-back in drilling activity. However, in general, the MLPs we own in client portfolios are entirely focused in the midstream3 segment and these businesses are not expected to cut distributions. In fact, the more diversified MLPs continue to increase distributions based on new projects being placed into service.

Recent confirmation came a few weeks back from Enterprise Product Partners L.P. (Ticker: EPD), the largest MLP and the bellwether for the nation’s midstream sector and one of the largest weightings in our clients’ MLP portfolios. Management announced they were raising their distribution this quarter at a

5.5% annualized rate. To give you a sense of how consistently this has occurred, this increase is the 45th consecutive quarterly increase and the 54th since the company’s IPO in 1998.

Excess industrial capacity is a great outcome for consumers but generally a bad thing for most investors. Since the shale revolution, we have witnessed a massive investment response by the midstream industry, which has dramatically increased capacity. While there has been a lot of capacity added, most industry experts recognize more is still needed.

Given that roughly 70% of midstream MLPs provide services to the natural gas arena, it makes sense to understand capacity conditions in this sub-sector. According to the US Department of Energy (DOE), from 1998 to 2013 capital outlays totaled more than $63 billion, and roughly 127 bcf/d (billion cubic feet per day) of pipeline capacity was added. Moving forward, estimates range from another $42-$45 billion in spending in order to add another 40 bcf/d of new capacity from 2015 to 2030.

The infrastructure implications of balancing new supply with increased demand likely means more investment is needed. While there are certainly areas more prone to overbuilding that is not the way we’d characterize the larger condition of broader midstream capacity. In general, more is needed not less.

Our portfolios primarily hold only midstream MLPs, which means they tend to follow more of a “toll-road” business model. As with toll-roads, their economics are more concerned with volume, specifically volume related to changes in overall energy demand. Importantly, changes in overall energy demand tend to be much more stable than changes in energy prices.

To be sure, large changes in energy prices can alter both supply and demand, which in turn, can affect volumes. In this case, lower prices means producers have less incentive to ‘push’ supply through the pipelines. While that is true and we have in fact already observed lower U.S. production, we should also note that many midstream contracts are fairly long-lived and the producers often pay for capacity whether they use it or not. Moreover, overall demand for energy in the U.S. tends to be fairly stable, if not expected to increase as a response to lower energy prices, which should help maintain a ‘pull’ of volume through the infrastructure.

Therefore, it shouldn’t be too surprising to learn the operating results for the core midstream businesses are in good shape even as we approach one-year into a dramatically lower oil price environment. Much of this has been generally confirmed by the absence of distribution cuts from any of the high quality infrastructure operators in our client portfolios. Moving forward, a few have hinted at lower growth prospects should prices stay lower for a longer period of time but many have actually increased their distributions in 2015.

Moreover, we’ve seen this movie before. Recall the financial crisis where oil prices dropped by $100/bl and the economy was in a pronounced contraction. In that environment only two pure midstream businesses cut their distributions. Of the fifteen largest operators, nine kept their distributions flat while six continued to grow every quarter! We’re not saying distribution cuts can’t happen in midstream businesses, but we do think history provides some support for our expectation that midstream MLPs will weather the current environment.

Over the past two years, valuation analysis has played a more explicit role in our asset allocation and risk management processes. Rewinding the film on our 2014 Capital Market Expectation (CME) process, one might ask: what happened, why did it happen, what have we learned and what are we doing about it?

As shown on the chart above like virtually every other asset class, MLPs were approaching fully-valued territory in March of 2014 (which is when we were completing our CME research). Over the course of just six months, MLPs valuations increased significantly. From a return perspective, they were +4% YTD as of March 2014. By the end of September, they were +25% YTD. Although MLPs carried the highest return expectation in our 2014 CMEs, we certainly did not expect them to rally that far beyond fair value that quickly. The MLP asset class effectively pulled forward three years of return into a 6-9 month period.

While MLPs clearly became expensive compared to trailing earnings, other metrics were not as daunting in September 2014. The income provided by MLPs as compared to Treasuries and other income producing assets was within a reasonable range of the historical average, and significantly better than the levels achieved by MLPs back in 2007.

Price-to-EBITDA1 for the Alerian MLP Index

Source: Bloomberg, Aspiriant. The Alerian MPL Index is comprised of 50 of the largest, publicly traded midstream master limited partnerships

1EBITDA=Earnings Before Interest, Taxes, Depreciation, and Amortization. It is often used as a proxy for cash flow. Data as of 10/30/15.

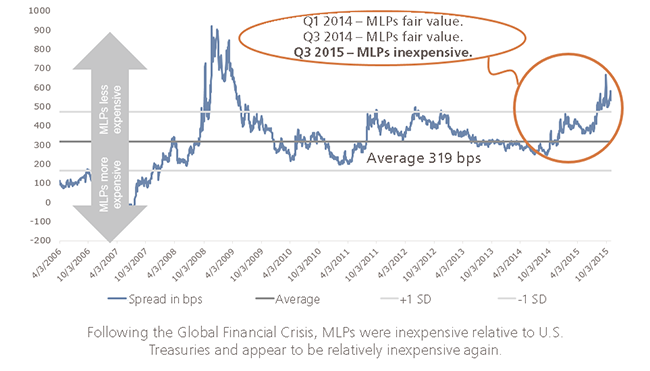

So, although we were concerned about our exposure to MLPs, we didn’t know whether or not valuations would remain high with the companies growing into those valuations or if the valuations would correct back downward. Clearly, MLPs not only reverted back through one standard deviation expensive, they have actually gone all the way back through fair value–making MLPs one of the only assets classes around that appears to possess both reasonable valuations and reasonable profitability.

Relative Valuationof MLPs to U.S. Treasuries

Source: Bloomberg, Aspiriant. Data as of 10/30/15.

*Vertical axis indicates MLP yield less 10-yr US Treasury yield also known as ‘spread.”

As an asset class, MLPs are appropriately characterized as being smaller and less diverse than most asset classes in which we invest. As a result, their valuations can move further and faster away from fair value than can the valuations of other developed asset classes.

Typical Asset Class |

MLPs |

|

| Market Capitalization | +$3 Trillion | >$500 Billion |

| Types of Investors | Institution & Individual | >Predominantly Individual |

| Investor Location | Global | >United States |

We believe this is precisely what has been happening. Indeed, from our lens MLPs have gone from one of the most expensive to one of the least expensive asset classes over the past ~12 months!

Although the experience has been painful, we have learned a lot about fundamentally attractive asset classes that can become susceptible to a “herd mentality.” Although MLPs appeared to be the most attractive asset class emerging from our 2014 CME process, with hindsight we should have acted with more caution rather than conviction when sizing the position in client portfolios given the valuation at the time, and we should have dollar-cost averaged into the position over a number of months. Also we should have the impact that seemingly unimportant news could have on a relatively thin asset class. Said another way, “headline risk” can have a much more pronounced impact on asset classes dominated by investors who react to news rather than invest with knowledge.

As mentioned earlier, we believe MLP valuations and profitability appear reasonable on both an absolute and relative basis4. So, we believe long-term investors should generally continue rebalancing back to their target weights. However, given the negative sentiment and other factors mentioned in this Market Perspective, we do not believe that investors should aggressively overweight the asset class. Negative headwinds may persist for a while longer, so this may not be the best time to augment the exposure. With that said, if valuations continue to fall and actually become “cheap,” then we may indeed recommend increased exposure down the road.

In an effort to avoid these kinds of whipsaw events in the future, we are enhancing our capital market expectation (CME) process to add an additional layer of risk management into our portfolio construction process. In advance of developing our 2016 CMEs, we plan to improve our process to better manage risk at the asset class level. Although the specific aspects of that process have yet to be fully determined, we will likely i) limit the maximum exposure our client portfolios can have to less developed asset classes and ii) raise our “conviction threshold” by decreasing the width of the valuation and profitability bands for less developed asset classes.

Over the long-term, we expect to be rewarded for dealing with the occasional growing pains of this sector. In our opinion, there is no other publicly-traded asset class that possesses the combination of growth, income and valuation characteristics that MLPs have today.

In looking at current expectations for our portfolios, the weighted yield in our MLP portfolio is about 7.1% based on closing prices through November 10th, and this very conservatively assumes no distribution growth. Additionally, while some well-respected asset managers in this sector are forecasting continued distribution growth of 8-10%, we have conservatively assumed a 3% growth rate in our expected returns. To sum up, we expect MLPs to generate an annualized return of +9% over the next 7-10 years, making it one of the most attractive asset classes today.

On the valuation side, as you’d expect after a 40% fall with little change in fundamentals, we think prices are looking attractive. On a relative basis, valuations are even more attractive as most financial assets around the world are expensive and will likely face valuation headwinds in the years to come. We don’t expect much, if any, valuation drag in the MLP space; and it’s possible, especially if oil prices stabilize, that we will see some tailwind from valuations as multiples stabilize.

It’s also worth noting the current losses we’ve experienced in MLPs over the last year are very near the level of losses incurred during the financial crisis. Investors need to remember that the two years immediately following the end of the financial crisis produced annualized total returns of 55% (e.g., 76% in 2009 and 36% in 2010) for MLPs. While there are no guarantees, we believe there will be an upside to this journey, and clients who have recently suffered large losses need to have the discipline to stay committed.

We don’t know when the volatility will end, but when it does the MLP businesses themselves and the publicly-traded partnership structure will prove resilient and durable. That’s not to say there aren’t any material ongoing risks related the MLP business model, but we think those scenarios are fairly low-probability given the increased role the MLP structure is expected to play in supporting U.S. energy independence, renewable energy and eventually natural resource exportation.

Although our long-term investment outlook remains positive, we recognize the current environment remains challenging. Uncertainty over upstream budgets and production volumes, negative fund flows, and potential interest rate hikes from the Fed have generated some fairly bitter sentiments on the sector that will likely take some time to dissipate.

In the meantime, we feel good about our portfolios collecting a stable source of above market yield (currently +450 bps over UST/S&P 500) while we wait for the pessimism to clear and for the sector to be valued in a manner more consistent with the operating fundamentals of these energy infrastructure businesses.

1Window-dressing occurs when fund managers remove poorly performing and/or add well performing securities before end of quarter holdings are made public in order to appear more favorable to investors.

2Upstream businesses are primarily focused on the exploration & production of energy and tend to be much more sensitive to changing commodity prices.

3 Midstream businesses are mostly focused on the processing, transportation and storage of energy and tend to be less sensitive to changing commodity prices.

4By “absolute,” we mean compared to their own history. By “relative,” we mean compared to other asset classes.

US Energy Information Administration, “Annual Energy Outlook 2015 with Projections to 2040,” April 2015

U.S. Department of Energy, “Natural Gas Infrastructure Implications of Increased Demand from the Electric Power Sector,” February 2015.

Interstate Natural Gas Association of America Foundation, Inc., “North American Midstream Infrastructure through 2035: Capitalizing on Our Energy Abundance,” March 2014

Gross, Richard et al. “MLPs This Time is Different.” Barclays Equity Research. August 2015

Important disclosures: Past performance is no guarantee of future performance. All investments can lose value. Indices are unmanaged and it is impossible to invest directly in an index. The volatility of any index may be materially different than that of a model.

Equities. S&P 500 is a market-capitalization weighted index that includes the 500 most widely held companies chosen with respect to market size, liquidity, and industry. The Russell 2000 Index measures the performance of the small-cap segment of the U.S. equity universe. It is a subset of the Russell 3000 Index representing approximately 10% of the total market capitalization of that index. It includes approximately 2000 of the smallest securities based on a combination of their market cap and current index membership. The MSCI EAFE Index (Europe, Australasia, and Far East) is a free float-adjusted market capitalization index that is designed to measure the equity market performance of developed markets, excluding the U.S. & Canada. The MSCI Emerging Markets Index is a free float-adjusted market capitalization index that is designed to measure equity market performance of emerging markets. The MSCI ACWI Index is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed and emerging markets.

Real Assets. S&P GSCI: The S&P GSCI® is a composite index of commodity sector returns representing an unleveraged, long-only investment in commodity futures that is broadly diversified across the spectrum of commodities. The returns are calculated on a fully collateralized basis with full reinvestment. Wilshire Global RESI is a broad measure of the performance of publicly traded global real estate securities, such as Real Estate Investment Trusts (REITs) and Real Estate Operating Companies (REOCs). The index is capitalization-weighted. The Alerian MLP Index is a gauge of large and mid-cap energy Master Limited Partnerships (MLPs). The float-adjusted, capitalization-weighted index includes 50 prominent companies and captures approximately 75% of the available market capitalization.

Want the latest wealth management tips, investment insights and Aspiriant news delivered straight to your inbox. Sign up for regular Fathom updates so we can send you the most relevant content you selected below.