Talk to us

Talk to us Investment Management

Second Quarter 2025 Insight

January 27, 2022

As the calendar page turns, many factors in the market and economy remain important to future economic growth. Below we lay out a few themes to watch, outside of new COVID-19 strains. Many of the issues relate to inflation and its impact on corporate earnings and valuations.

The economic rebound has been profound. Fiscal policy was a key catalyst, injecting over $5 trillion, or 25% of GDP, in a little over a one-year period. To put this in perspective, fiscal support during the Global Financial Crisis was only 5% of GDP. In addition, significant amounts of pandemic era stimulus went directly to households, providing tremendous support to consumers, but also putting significant pressure on inflationary trends.

The market has moved quickly past the disappointment of the unsuccessful attempt to pass the Build Back Better Act. The mid-term elections provide a difficult environment to move forward on major legislation. The lack of additional fiscal spending could help to curb inflation given already strong economic growth.

The Federal Reserve has many competing factors to consider as it determines policy moves going forward. The Fed ended 2021 by acknowledging a change in policy. Its tone is more hawkish, but maybe not to the point of tightening. The market is not yet concerned the Fed waited too long. However, if the Fed has waited too long, it may have to move faster than the market expects, which has caused problems during past periods of economic growth.

The Fed is tapering bond purchases with a goal to end them in the coming months. Yet unknown is when it will start reducing the size of its balance sheet and what the pace and timing will be compared to interest rate increases. Reduction in the balance sheet is a form of tightening monetary policy that contributed to a slowdown in 2018.

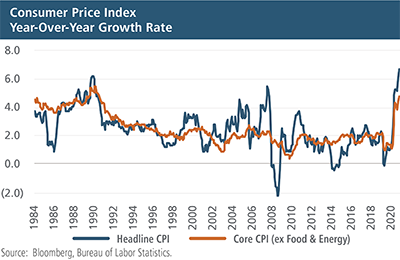

Market expectations have increased over the last quarter to three interest rate hikes during 2022. While the most recent inflation number may not be a surprise, there’s growing concern inflation may continue to linger longer than the Fed originally believed.

Job market gains continue and are improving at a faster pace than expected. The unemployment rate has fallen fast to 3.9%, and the Fed’s December forecast is for the rate to end 2022 at the 3.5% low seen in early 2020. In addition, annual wage growth has averaged over 5% during the last six months, and the labor force participation rate continues to edge higher. These numbers lead to hope this job market is one pillar to creating a self-sustaining economic recovery.

Important Disclosures

Aspiriant is an investment adviser registered with the Securities and Exchange Commission (“SEC”), which does not suggest a certain level of skill and training. Additional information regarding Aspiriant and its advisory practices can be obtained via the following link: https://aspiriant.com.

Investing in securities involves the risk of a partial or total loss of investment that an investor should be prepared to bear.

Any information provided herein does not constitute investment or tax advice and should not be construed as a promotion of advisory services.

The views and opinions expressed herein are those of Aspiriant’s investment professionals as of the date of this article and may change at any time without prior notification. The charts and illustrations shown are for information purposes only.

All information contained herein was sourced from independent third-party sources we believe are reliable, but the accuracy of such information is not guaranteed by Aspirant. Any statistical information in this article was obtained from publicly available market data (such as but not limited to data published by Bloomberg Finance L.P. and its affiliates), internal research and regulatory filings.

Want the latest wealth management tips, investment insights and Aspiriant news delivered straight to your inbox. Sign up for regular Fathom updates so we can send you the most relevant content you selected below.