Talk to us

Talk to us Uncategorized

Celebrating “Money Tales”: Inspiring Financial Conversations

September 14, 2020

A global pandemic and collapse in incomes. Negative real interest rates. Mounting debts across most segments of the economy. Trillions of new paper money. Rising geopolitical tensions. With these unusual circumstances comes a widening range of outcomes for the economy and financial markets.

Deflationary impulses in the near term could give way to inflationary momentum in the more distant future. The ultimate trajectory of the economic recovery rests on ongoing policy initiatives, scientific advances and behavioral responses by households and companies. Given these heightened uncertainties, we believe investors will be well-served by holding assets that are resilient to the multiple scenarios that may unfold in the years ahead. Gold, in our view, is one of those assets and ideally suited for these turbulent times.

To stimulate economic growth over the past decade and especially now, the Federal Reserve (and other developed world central banks) has pushed short- and long-term nominal interest rates to approximately 0%. Futures markets suggest this condition will last for at least the next few years. Given the likelihood of an uneven and protracted recovery ahead, together with the massive dent any material interest rate increase would place on our already strained fiscal position, we also believe interest rates will be anchored near zero for quite some time.

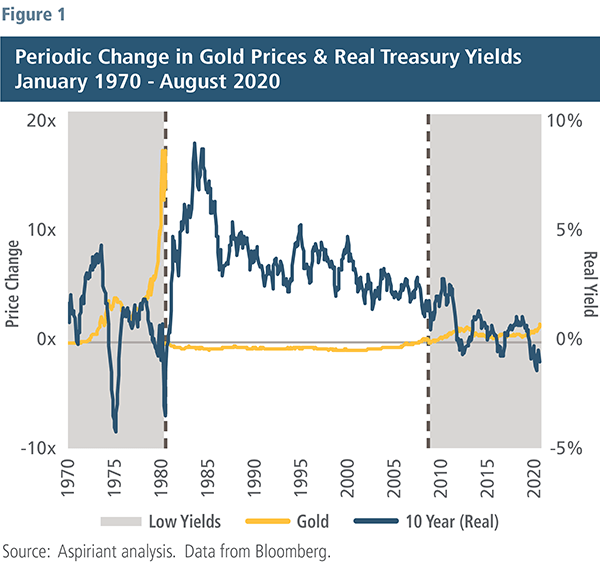

Like other commodities, gold does not provide its owners any recurring cash flow or income. Because of that unique characteristic, gold tends to do well when investment substitutes such as cash or government securities offer a low inflation-adjusted or real rate of return. Over the past 50 years, gold generated an annual real return of 14.2% (or 19.2% in nominal terms) when the opportunity cost of holding it was unusually low, like today. Figure 1 shows two similar periods in gray, the 1970s and the years since the start of the Global Financial Crisis (GFC).1

Conversely, gold prices have largely stagnated in periods when real returns on similar, store of value assets were moderately positive or higher (the middle section of Figure 1). In 1980, the price of gold was $653 an ounce. Twenty-eight years later, the price had increased by only $70 an ounce, translating into annual nominal and real returns of 0.4% and -3.0%, respectively. During that period, the average real yield on a 10-year U.S. Treasury Note was 3.6%.

Coming into the year, U.S. government spending gaps and debts were at the their most extreme levels of the past 75 years. Unfortunately, the pandemic will only further impair our country’s financial health. The Congressional Budget Office forecasts the U.S. 2020 budget deficit will approach 20%, a shortfall last touched during World War II. Furthermore, U.S. government debt-to-GDP is anticipated to reach near 120% in the next year, a burden that not only rivals the war era but is also roughly double the ratio that existed before the onset of the GFC in 2008.

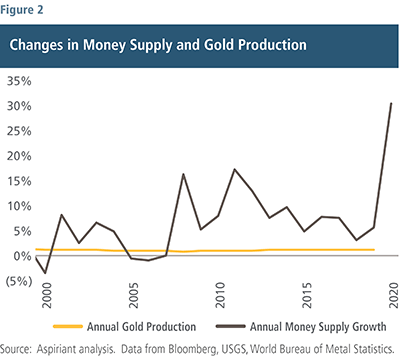

Given the acceleration in the size of our budget deficits, and without a material rise in interest rates, private markets participants are unlikely to absorb all of the soaring issuance of government securities. To that end, we believe substantial debt monetization by the Federal Reserve or money printing will be necessary to deal with these elevated government financing needs. Large increases in the money supply, often precursors to future inflation or currency weakness, have historically been highly correlated to gold prices. Since the end of the Bretton Woods framework2 (of fixed exchange rates) in 1971, a jump in the money supply of greater than 20% has often coincided with strong positive movements in the price of gold. Over the 12 months ending June 30, 2020, the money supply in the U.S. has surged by over 30%, with gold prices climbing by 26%.

Distinct from paper currencies, gold is a finite resource, and its supply is not easily manufactured by a simple electronic transfer. Over the past 20 years, as highlighted in Figure 2, the annual production of gold has equaled roughly 2% of existing supply. Substantial new discoveries are increasingly rare, with production expected to become even more constrained in the years ahead. Long development timelines, remote sites with little surrounding infrastructure, and newly attuned concerns about destructive mining techniques are among the factors that will limit future production. In contrast, the money supply (defined here as physical currency, demand deposits and checking accounts, as well as traveler’s checks) has increased, on average, by 8% per year over this same period, with more pronounced spikes around recessions, including the current one. If history is any guide, then the recent and ongoing spike in the money supply, coupled with the exceedingly controlled production of gold, should help steer gold prices higher.

Commodity prices tend to adjust quickly to changing market dynamics, including shifts in supply and demand. Conversely, the price of final goods and services vary on a delayed basis, with disparate effects on corporate cash flows and financial security interests. Accordingly, commodities, gold specifically, have proven to be reliable hedges in periods of rising inflation. During the 1970s, gold returned 30% annually (nominal). Over this same interval, the S&P 500 and the Bloomberg Barclays Aggregate advanced 1.6% and 6.1%, respectively, while the consumer price index averaged 7.4%.

Some will argue that this same expectation of ascending prices did not materialize in the years following the GFC, and that undermines the case for owning gold now. We disagree.

First, some of the disinflationary pressures of the last several years, like globalization and lower taxes, are likely to revert in the years ahead. For example, over half of the respondents in a recent PricewaterhouseCoopers survey of chief financial officers indicated a plan to develop alternative sourcing options for their supply chains,3 likely heralding a shift to greater national self-sufficiency and an end to the more integrated and cheaper solutions of years past. Several members of the European Union have proposed instituting a tax on select gross revenues of large (and predominantly U.S.) digital companies. Similarly, the Democratic presidential nominee, former Vice President Joe Biden, has released a tax plan that would bump the corporate tax rate from 21% to 28% and set minimum corporate taxes for both domestic and foreign income.

Second, the level of central bank intervention today dwarfs the activity in the GFC. In the last five months, the Federal Reserve’s balance sheet has increased by about $3 trillion, an amount it took almost five years to amass during the GFC.

Third, current and future central bank asset purchases should have a more direct link to spending on goods and services and, therefore, have more significant inflationary implications than what materialized during and after the GFC. Back then, the Fed was steadfastly determined to recapitalize financial institutions and embarked on multiple rounds of quantitative easing to satisfy that objective. In doing so, its purchase of U.S. Treasurys and mortgage-backed securities (assets) largely just boomeranged back to the other side of its accounting ledger in the form of excess reserves (liabilities) held by banks and other depositary institutions. With materially tighter lending standards, this liquidity simply did not flow into the economy via loans and credit, and consumer spending and business investment remained fairly muted. Yes, financial asset inflation did occur, but the gains disproportionately accrued to the affluent, and their propensity to spend on each marginal dollar of wealth is exceedingly low. As the Fed finances a large portion of burgeoning government spending in the years ahead, trillions of dollars should cascade, with much less friction, into the economy and have a more pronounced effect on price levels.

One last point on gold and the GFC — While gold did come off its highs of about $1,900 an ounce a few years after the beginning of that recession, it settled in the $1,200 to $1,300 an ounce range, a level that was 50% higher than where it was before start of the GFC. If an investor timed their exit perfectly, then buying gold before the start of the previous recession generated a return in excess of 100%. Otherwise, the realized gain was a lower, but still respectable, 50%.

For years, a number of enduring pillars underpinned the dollar’s strength and central role in the global economy. Among these foundations were the dynamism and size of the U.S. economy, stable and long-standing democratic and legal traditions, deep and liquid capital markets, the absence of an economic and military rival, and a global financial architecture heavily reliant on dollar funding and trade settlement. More recently, interest rate differentials relative to other G4 or developed market reserve currencies also buoyed dollar demand. While these conditions served to make the dollar the world’s currency of choice, its global hegemony is not permanent.

With the onset of the pandemic, the positive interest rate spread U.S. government securities enjoyed for much of the last several years has now largely evaporated. A number of the countries or regions that run current account4 surpluses and channel those trade flows into dollar assets to forestall currency appreciation are pressing ahead with their own large fiscal stimulus programs. This largesse may lead to greater imports, lower surpluses and less demand for U.S. assets. Relatively disjointed virus testing and contact tracing, coupled with haphazard reopening protocols, may also mire the U.S. in a more prolonged economic recovery and burden it with even greater debts than other countries. Divisive politics, persistent trade gaps, recurring geopolitical skirmishes and the unrelenting rise of China are other factors that can erode confidence in the dollar over time. To that end, the dollar is off 7% against a traded weighted basket of currencies since March.

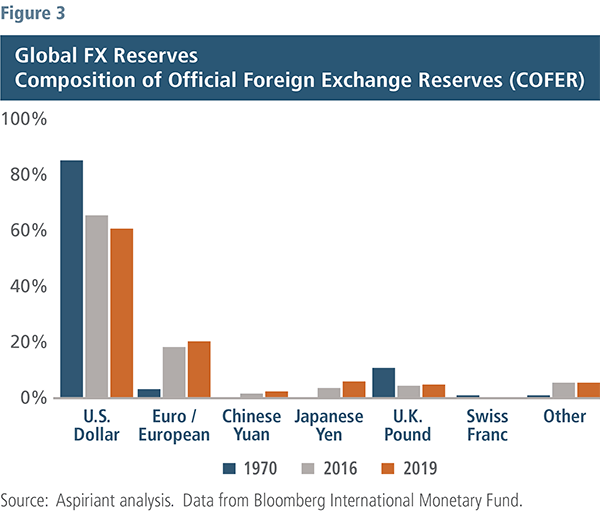

Further weakness in the dollar and any accelerated desire to diversify away from dollar assets would, undoubtedly, have profound implications for financial markets. Foreign investors, for example, hold approximately 30% of the U.S. Treasury market. Among the largest holders of this debt are international central banks. Today, the U.S. accounts for a little less than 25% of world production, but dollar assets account for 61% of central bank reserves, as represented by the orange bar in Figure 3. That has dropped over the past 50 years, from a shade below 85% in 1970, as shown by the blue bar.

In the absence of any strong alternatives in the near-term, gold should benefit from this shift. Gold has long been used as a currency, and only in the past several decades has its use waned with the rise of paper or fiat currencies. Moreover, gold, like other commodities, is priced in dollars in global markets and generally benefits as the dollar weakens. The Russian and Chinese central banks, perhaps portending a larger trend, have added about 2,000 tons of gold to their reserve holdings, an increase of approximately 85% in the past five years.

Investing is challenging in the best of circumstances. Add in the profound shifts in government policy, along with generational health and economic anomalies, and the exercise becomes exponentially more difficult. Accordingly, holding assets that are responsive to the present uncertainties and the expanding range of possible endpoints is vitally important. Gold, a peculiar holding under normal circumstances, possesses attributes that are now suddenly beneficial. It is a physical asset with limited supply and long used by investors to store wealth in times of acute ambiguity, whether that is related to inflation, economic growth or world events. In short, today’s intersection of elevated risks, multiplying unknowns and irregular policy is gold’s moment to shine.

11970s period was from January 1970 through June 1980; the years since the start of the Global Financial Crisis period are from November 2008 through August 2020.

2To ensure exchange rate stability, prevent competitive devaluations and promote economic growth, delegates from 44 Allied nations met in Bretton Woods, N.H., in July 1944 and established a new international monetary system. Under this new framework, currencies were pegged or fixed, within a 1% band, to the dollar, and the dollar was linked to gold at the rate of $35 per ounce. In August of 1971, the United States unilaterally terminated convertibility of the dollar to gold, effectively ending the Bretton Woods system.

3PwC’s COVID-19 CFO Pulse, May 11, 2020.

4The current account represents a country’s net trade in goods and services, net earnings on cross border investments, and net transfer payments (such as foreign aid).

Important Disclosures

Aspiriant is an investment adviser registered with the Securities and Exchange Commission (SEC), which does not suggest a certain level of skill and training. Additional information regarding Aspiriant and its advisory practices can be obtained via the following link: https://aspiriant.com.

Investing in securities involves the risk of a partial or total loss of investment that an investor should be prepared to bear.

Any information provided herein does not constitute investment or tax advice and should not be construed as a promotion of advisory services.

The views and opinion expressed herein are those of Aspiriant’s portfolio management team as of the date of this article and may change at any time without prior notification. Any information provided herein does not constitute investment or tax advice and should not be construed as a promotion of advisory services.

Past performance is no guarantee of future performance. All investments can lose value. Indices are unmanaged and you cannot invest directly in an index. The volatility of any index may be materially different than that of a model. The charts and illustrations shown are for information purposes only. All information contained herein was sourced from independent third-party sources we believe are reliable, but the accuracy of such information is not guaranteed by Aspirant. Any statistical information in this article was obtained from publicly available market data (such as but not limited to data published by Bloomberg Finance L.P. and its affiliates), internal research and regulatory filings.

S&P 500 is a market-capitalization weighted index that includes the 500 most widely held companies chosen with respect to market size, liquidity and industry. Bloomberg Barclays US Aggregate Bond index is a broad-based benchmark measuring investment grade, US dollar-denominated, fixed-rate taxable bonds.

Want the latest wealth management tips, investment insights and Aspiriant news delivered straight to your inbox. Sign up for regular Fathom updates so we can send you the most relevant content you selected below.