Talk to us

Talk to us Investment Management

Second Quarter 2025 Insight

November 16, 2021

Powerful pent-up demand and massive fiscal and monetary stimulus have led to strong corporate earnings and substantial gains across all asset classes. However, inflation, long dormant, has risen to levels unmatched for much of the past 25 years. For now, this recent surge in prices has not imperiled the economy or markets as long-term inflation expectations remain anchored to levels observed over the past several years.

Investors, however, must not get complacent and assume the future will repeat the past. We see inflationary pressures building across the supply chain. A shallow labor pool and business underinvestment are particularly worrisome and require closer examination.

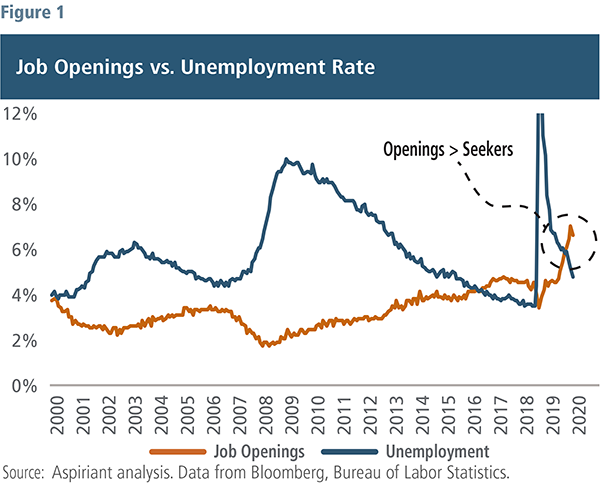

Labor is a key factor of production, and the labor market in this country and others appears quite tight. Job openings and unemployment tend to converge later in the economic cycle and widen during recessions. And in almost all cases, the number of unemployed people exceeds the number of job openings. That historical relationship broke at the tail end of the last expansion in 2017/2018, but not by much. Today, we have a record number of job openings, equaling 6.6% of the labor force, against an unemployment rate of 4.8%, as shown in Figure 1, creating the largest divergence between job openings and the unemployed on record.

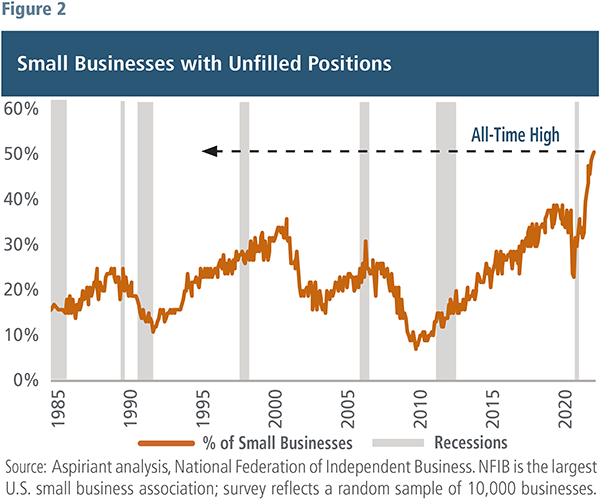

Business owners, not surprisingly, are very concerned with the labor shortage. The number of small businesses with positions they are unable to fill is at an all-time high of more than 50% (Figure 2). One thing to recognize, and perhaps this skews the data in Figure 1 and partially explains the frustrations of small businesses, is about 5 million workers left the labor force since the start of 2020. Significant government transfers or unemployment benefits, early retirements, opposition to vaccines, lingering health concerns and child-care obligations are among the reasons for this exodus.

When and how many of these workers return to the labor force is hard to know, but the absence of that many people, at a time of strong consumer demand, is clearly amplifying the challenges confronting businesses. If these departed workers don’t return to the labor force, very little slack in productive capacity will remain and hiring pressures will only become more pronounced, especially as manufacturers attempt to ramp up production and services to historically normal levels.

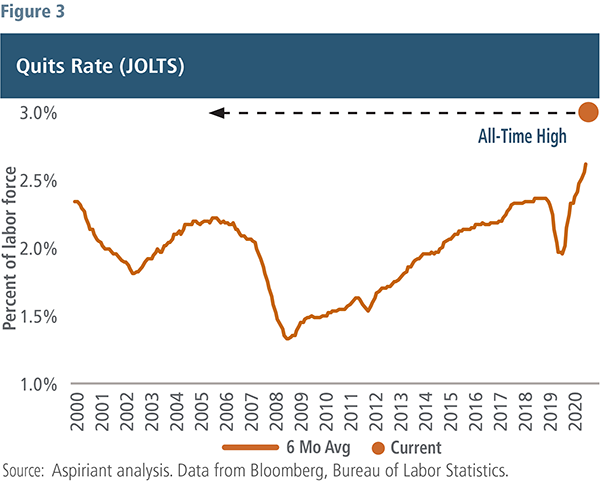

With a tight labor market, the relative bargaining power of workers is shifting. Workers are more confident than ever of their employment prospects and are quitting jobs at a record rate.

In Figure 3, we look at a six-month average to smooth out the month-to-month gyrations, with the current month marked by the orange dot. As you can see, both the six-month average of 2.6% and current one-month measure of 2.9% are at historical highs. Interestingly, resignations are highest for mid-career employees, those aged 30 to 45. With the transition to remote or hybrid work, the presumption is employers prefer higher skilled workers that require little onsite training, thereby giving workers in this cohort more flexibility and options than they otherwise had before. In contrast, resignation rates for entry-level and older workers have declined over the past several months.

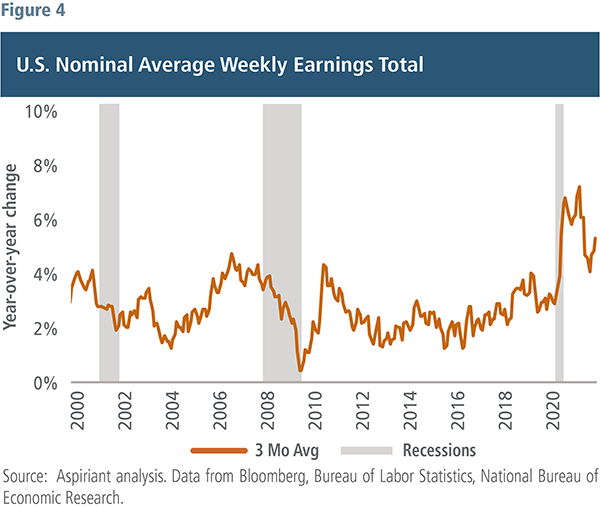

Higher turnover creates a number of adverse outcomes for employers, including the loss of institutional knowledge and productivity, and more directly forces business owners to spend additional money to retain existing employees and attract new ones. And we are seeing some of those higher costs in the compensation data. Figure 4 illustrates the three-month average change in weekly earnings from the prior year since 2000. Recent measures show earnings spiked 7.3% in January with gains settling down to a still high 5.9% in September. Should the labor market continue to tighten, we would expect to see this trend persist and likely make higher inflation of goods and services a bit stickier since labor is one of the largest expenses for most businesses.

But we’re not just facing labor shortages and higher wage costs. The problems are much broader than that.

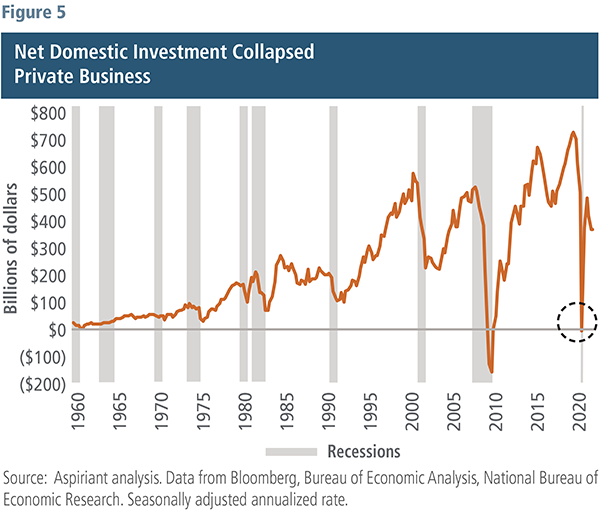

Figure 5 displays net domestic investment by U.S. private businesses in factories, buildings, tools, machinery and equipment. We’re using the data as a proxy for overall business investment in the U.S. and abroad.

As shown, business investment collapsed in the early part of the pandemic. Investment essentially fell to zero in the second quarter of 2020. The Global Financial Crisis (GFC) was the only other time in the past 50 years with a worse result. And while recent investment activity has rebounded, it’s still 40% below pre-pandemic levels. Since there’s typically a lag between capital investments and when productive capacity comes online, underinvestment could continue to restrain supply in the months ahead.

Figure 6 shows global shipping routes are also capacity constrained. The Baltic Dry Index represents the cost manufactures must pay to ship a standard cargo container across one of 23 global shipping routes. That cost is up over 250% year-to-date.

Some of the world’s largest ports-of-entry are also experiencing dramatic congestion. For example, the Los Angeles and Long Beach ports handle 40% of all shipping containers entering the United States. Currently, a record-high 100 ships are waiting offshore to unload their cargo.

In addition, flatbed long-hauling freight rates are up 28% year-over-year. And the industry is coping with an estimated shortage of 80,000 truck drivers.

Industrial metals used in construction and manufacturing have, in a sense, become “precious.” Inventories of copper, aluminum, lead, tin, zinc and nickel are at or near all-time lows. As a result, prices are testing all-time highs in order to fill demand for homes, cars and other durable household goods. Moreover, underinvestment in recent years will require significant new capital and plenty of lead time to bring sufficient capacity online. So, we doubt metals prices will cool anytime soon.

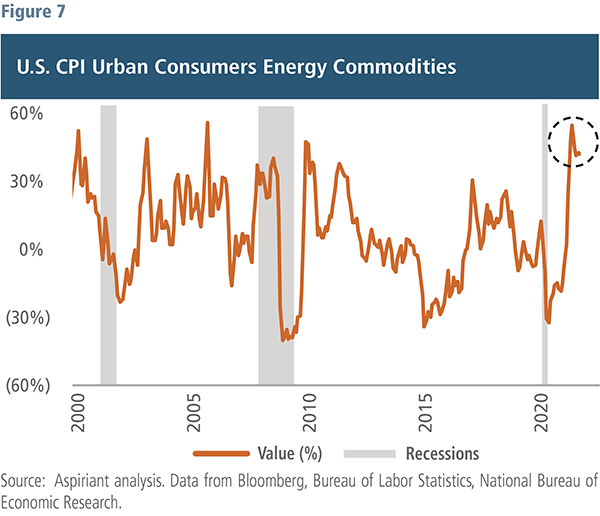

Meanwhile, the cost of energy needed to transform raw materials into finished goods is also skyrocketing. Energy prices are typically quite volatile, as you can see across the two decades on Figure 7. But the rapid ascent from trough to peak is as steep as the recovery after the GFC.

Inventories of oil, coal and natural gas have fallen dramatically over the past several months as demand has retraced losses from the pandemic. Moreover, the movement to renewable energy sources as investors embrace environmental, social and governance (ESG) factors will likely keep fossil fuel prices elevated. And, while energy prices are excluded from Core CPI, energy is directly or indirectly necessary to the production of virtually every good and service available.

The economic, employment and financial markets recoveries from the depths of the COVID-19 recession have been nothing short of remarkable. To date, all three areas are near or above their pre-pandemic levels in early 2020. However, as progress continues, the uniformity across these three dimensions may splinter. Ongoing supply chain dislocations are contributing to demand and supply imbalances that could push long-term inflation expectations higher and force a more aggressive policy response from the Federal Reserve (accelerated and larger rate interest hikes). Conversely, withdrawal of fiscal stimulus, along with eventual reversal of labor and capital shortages could moderate economic activity and current wage increases.

In either outcome, we expect a more uncertain future and, in turn, more volatile markets. Investors should prepare for these risks and hold portfolios that have resiliency to these evolving conditions. Read more about it in our Fourth Quarter 2021 Insight.

Important Disclosures

Aspiriant is an investment adviser registered with the Securities and Exchange Commission (“SEC”), which does not suggest a certain level of skill and training. Additional information regarding Aspiriant and its advisory practices can be obtained via the following link: https://aspiriant.com.

Investing in securities involves the risk of a partial or total loss of investment that an investor should be prepared to bear.

Any information provided herein does not constitute investment or tax advice and should not be construed as a promotion of advisory services.

The views and opinions expressed herein are those of Aspiriant’s investment professionals as of the date of this article and may change at any time without prior notification. The charts and illustrations shown are for information purposes only.

All information contained herein was sourced from independent third-party sources we believe are reliable, but the accuracy of such information is not guaranteed by Aspirant. Any statistical information in this article was obtained from publicly available market data (such as but not limited to data published by Bloomberg Finance L.P. and its affiliates), internal research and regulatory filings.

Want the latest wealth management tips, investment insights and Aspiriant news delivered straight to your inbox. Sign up for regular Fathom updates so we can send you the most relevant content you selected below.